Embedded insurance refers to insurance products that are purchased as part of a package with a service or item. The approach is not new: for example, a landlord on Airbnb automatically receives liability insurance that covers him against damage or theft of guests’ property, among other things. Another well-known example is cell phone insurance, such as that offered by Swisscom: when a new device is purchased in a Swisscom store, it can be optionally insured against various types of property damage.

Functionality of Embedded Insurance

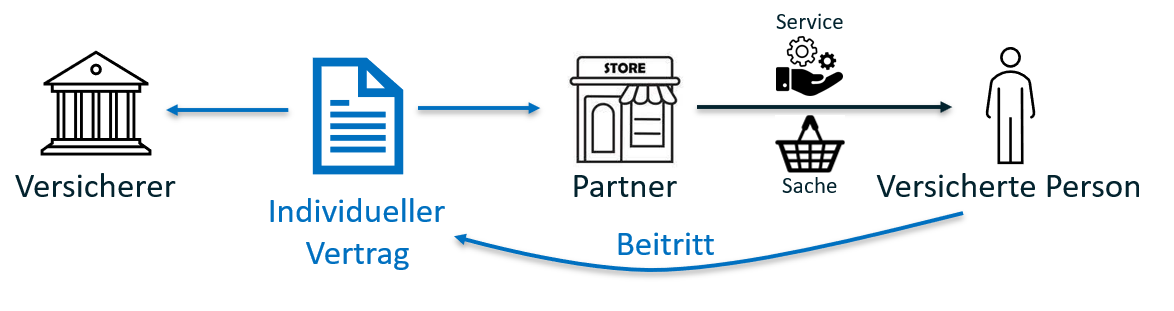

Unlike conventional insurance policies, embedded solutions cannot be taken out separately from the service or item. In some cases, the customer is not even aware of the insurance cover – at least until a claim is made, as is the case with Airbnb cover mentioned above. In terms of insurance, embedded products are usually covered by collective contracts. The insurance partner, i.e. Airbnb or Swisscom in the examples mentioned, is the policyholder. Insured persons, i.e. the landlord or cell phone owner, then join the collective contract.

Insurance companies expect a great deal of growth from embedded solutions, not least through the use of the partners’ new sales channels. Accordingly, many are developing new offers together with partners and testing them on the market.

The Challenges

Due to various peculiarities of embedded products, there are a number of challenges in their implementation and operational processing, which affect IT in particular. At its core is a “balancing act” between individualization and standardization that must be mastered: the contract between the insurance company and the policyholder (the partner) must be able to reflect the individual needs of the partner, but the conditions, benefits and premiums for the insured persons are highly standardized within the contract.

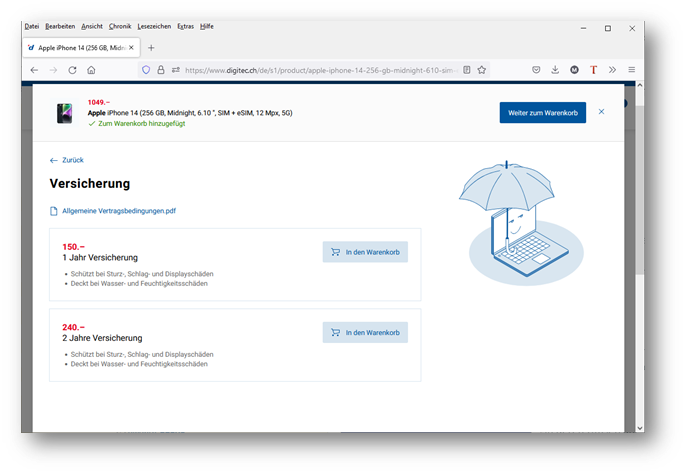

Screenshot Embedded Insurance bei Digitec

At least initially, a high degree of flexibility is required when defining and rolling out the products. The partners want to be able to integrate new solutions quickly and, based on their experience in the market, be able to make adjustments and extensions together with the insurers.

It must also be possible to map a wide variety of products in different sectors; the requirements differ significantly depending on the partner and the type of product they offer. This also applies to billing Do the insured persons receive the premium invoices or is billing handled in summary form by the partner, who then passes them on depending on the product? Are the products tied to a fixed term or extended on a recurring basis? Is billing done once, monthly or annually?

The interface from the partner to the insurer must also be made available. After all, the partner is in charge when new insured persons join and usually also when individual insured persons make changes or leave. How does the insurer receive the relevant entries and changes? This is often done manually via spreadsheets, i.e. the partner sends the insurer an Excel spreadsheet with all new entries every month, for example. In return, the insurer then creates a statement based on this data, also manually. Operating such a manual interface is inefficient, error-prone and unattractive for the employees involved. In addition, the data is difficult or impossible to evaluate, which means that further business potential is wasted.

This is a pity and avoidable, as we show below.

Digital implementation with Consor Universal’s Object Manager

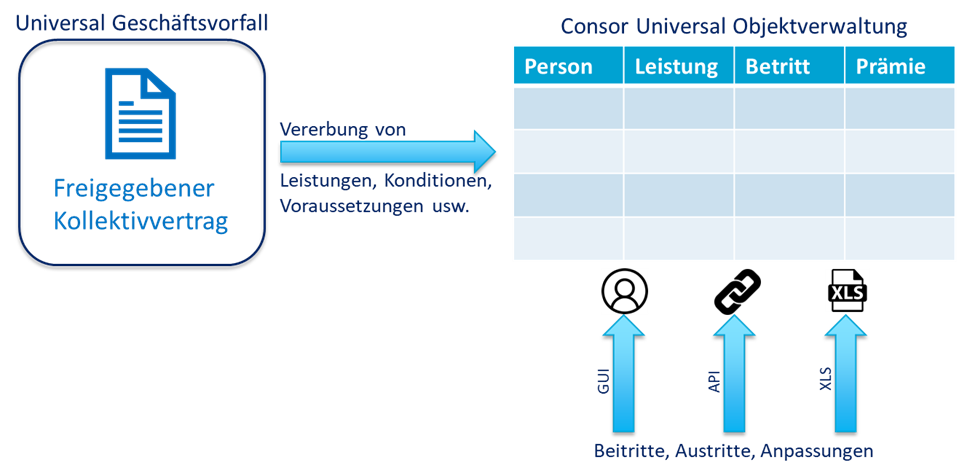

Property management is a tried-and-tested module from Consor Universal. Originally developed for large property insurance contracts, our customers are increasingly using it for embedded insurance in order to serve their cooperation partners better and more efficiently. We have also extended the module specifically for embedded insurance.

The contract with the partner is created and released as a regular business transaction with the usual flexibility of Consor Universal. However, the insured persons are outsourced to object management. When a new person joins, the rules defined in the business transaction, e.g. those for pricing or entry requirements, are inherited and applied to the person. For example, the person’s premium can be calculated or membership can be refused because the requirements are not met.

Embedded Insurance with Consor Universal

Object management is seamlessly integrated into Consor Universal. Both the business transactions and the objects can be fully modeled: Business users define the entire business logic, the data structures, the output and also the user interface using the Consor Universal design engine. In this way, data that varies by product and industry (e.g. personal details, addresses, premiums, insurance sums, details of the cell phone model, etc.) can be kept in object management.

The objects are managed historically. They can be manipulated in 3 different ways:

Manually via the Consor Universal user interface.

From peripheral systems via the API. Partner applications can report entries, adjustments and exits directly and online. Reporting by file with subsequent batch processing is also supported.

By uploading an Excel file with the corresponding changes.

Last but not least, contracts can also be billed via Consor Universal’s inventory management.

Conclusion

Embedded insurance offers insurance companies many exciting opportunities. However, with increasing maturity and growing volumes, it is important to integrate cooperation partners quickly and digitally. Insurance companies must also ensure that they can maintain and bill their offers efficiently. Consor Universal offers an ideal solution for this with property management.

Would you like to know more? Then get in touch with us.