Since the 1970s, the insurance industry has been one of the leading sectors in terms of the use of information technology. From the mainframe for billing policies to the mobile app for the insured individual – digitalization has permeated all processes and aspects of the insurance industry for more than 50 years.

Industrial insurance, with its complex risks and specialized customers, has long been an exception in this respect. How can you standardize and automate something that has an individual character per se? Today, however, industrial insurance is also faced with the challenge of adapting to new technologies in order to remain competitive.

New perspectives through platforms

Traditionally, industrial insurers have segmented their customers according to company size and industry affiliation in order to better understand risk profiles and customer needs. But with the advent of digital platforms, the focus is shifting. Platforms such as Corify (https://www.corify.de/) enable a digitalized exchange between insurers and brokers. This leads to a certain standardization of processes and data, which in turn increases efficiency and improves interaction between the parties.

The future of IT architectures for industrial insurance

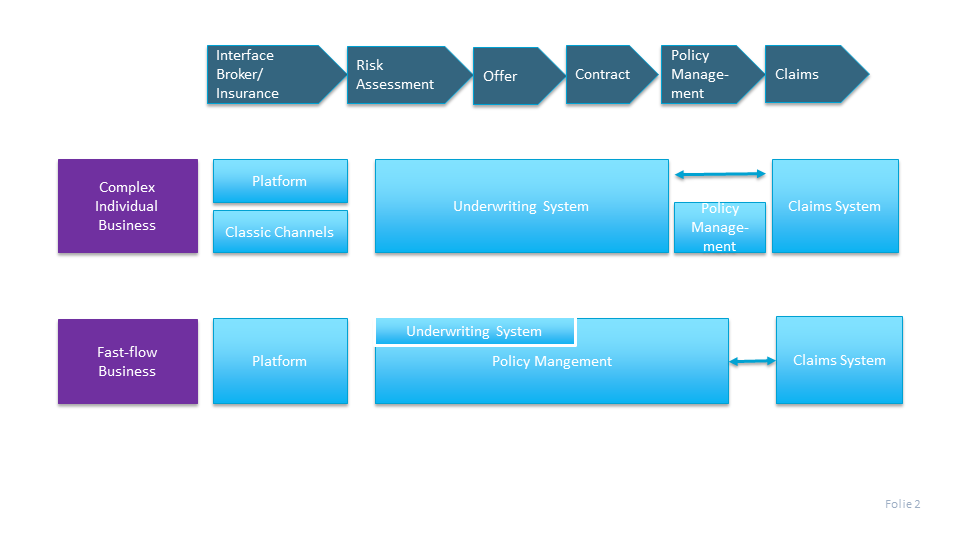

If we look at the effects of these changes on the IT architectures of industrial insurers in particular, it becomes clear that different business models also place different demands on IT systems. For example, the highly complex individual business requires flexible and individualized IT support, while the fast-flow business relies on standardization and automation.

The challenge for the IT architecture is to meet both requirements. An attempt can either be made to master this balancing act by using a single system to cover all the needs of the different segments. Or you can avoid the balancing act by adopting a two-platform strategy: a standardized, automated platform for the fast-flow business and an individual, flexible platform for the industrial business.

Individual, flexible needs in the industrial business

The renowned consulting firm Oliver Wyman, which specializes in the insurance industry, has given this question some in-depth thought. See “St. Gallen Trend Monitor for Risk and Financial Markets” issue 3/23 of the Institute of Insurance Economics, University of St. Gallen. The authors from Oliver Wyman suggest using a broad underwriting platform that can map the complexity of individual business.

This platform should be flexible enough to support individual products and processes, while at the same time enabling seamless integration with upstream and downstream systems such as the partner system or the collection/disbursement system. In fast-flow business, on the other hand, the core processes should be integrated in policy management, with the underwriting system only taking on a subordinate, supporting role.

Today, the common core systems for insurers’ portfolio management are based on the second design principle (efficient portfolio management for fast-flow business). However, this does not meet the requirements of individual business. The flexibility required for individual business must therefore be mapped in an upstream, separate underwriting system that is built according to the first design principle.

Underwriting Platform

Future Outlook

individual business and in many cases still uses Excel for pricing and Word for creating contracts. With the emergence of digital platforms at the interface between insurers and brokers, the form of interaction with sales partners will continue to develop. This will increase the networked exchange of data and the relevance of technical standards in service agreements.

The experts at Oliver Wyman emphasize the importance of seamless integration of digital interfaces both externally and in internal processes. This is the only way for insurers to meet the requirements of an increasingly digital world and secure their long-term competitiveness.

If you would like to know how Consor Universal can support you with digitalization, please contact us.